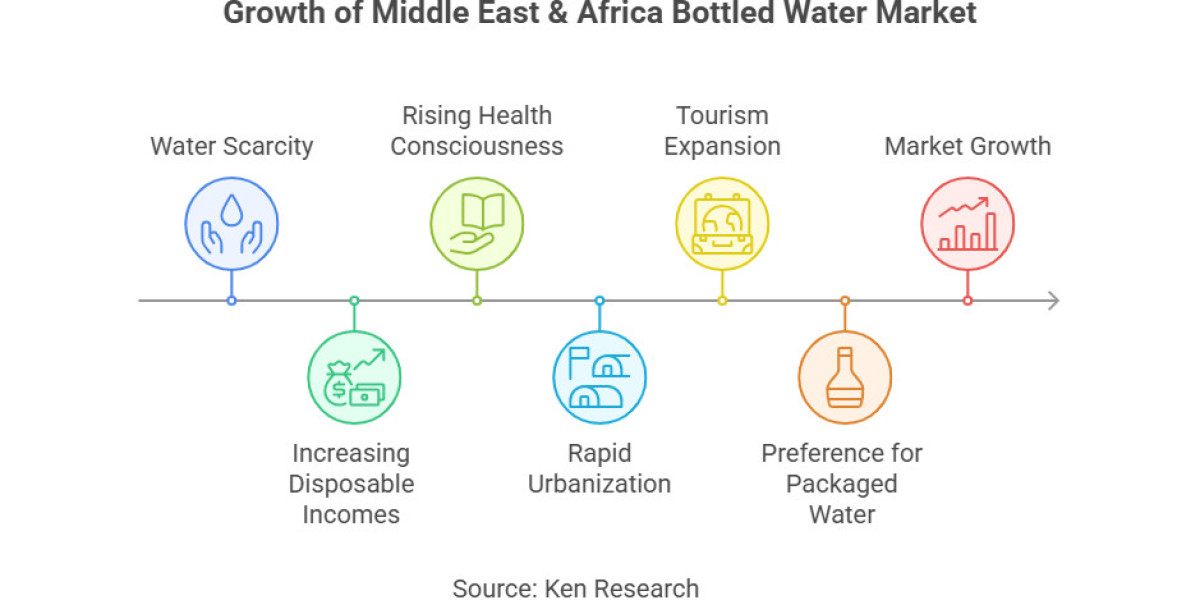

The Middle East & Africa Bottled Water Market is experiencing robust growth, driven by factors like water scarcity, increasing disposable incomes, and rising health consciousness. Valued at approximately US $13 billion based on past five-year historical data, this market reflects a strong upward trajectory supported by rapid urbanization, tourism expansion, and a heightened preference for packaged drinking water.

Key Market Drivers

Water Scarcity and Quality Concerns

Widespread water stress across North Africa and the Middle East has accelerated bottled water consumption as consumers prioritize safe drinking options amid unreliable municipal supplies.

Health and Lifestyle Trends

The pursuit of wellness and fitness across MEA has fueled demand for purified, mineral, and functional bottled water. Consumers now prefer health-oriented variants over sugary or carbonated beverages.

Tourism and Hospitality Growth

Tourism hotspots like the UAE, Egypt, and South Africa have boosted demand via hotels, airlines, and resorts—evident in Mai Dubai being the preferred water brand for Emirates passengers.

Urbanization and Retail Expansion

Rising urban populations in MEA regions have propelled bottled water sales through supermarkets, convenience stores, and online retail platforms.

Emerging Trends

Premium & Mineral Water Solutions: Brands such as Sohat (Lebanon), Arwa (UAE), and Ambo (Ethiopia) are capitalizing on natural sources and mineral-rich profiles to target discerning consumers.

Sustainable Packaging Innovations: Pet plastic usage faces scrutiny, pushing manufacturers toward lightweight bottles, recycled PET, and eco-friendly packaging alternatives.

Flavor & Functional Variants: Sparkling and flavored water products—like Arwa Fruits—are gaining traction for their novelty and taste appeal.

Direct-to-Consumer Channels: Brands increasingly adopt D2C strategies via digital platforms, enabling personalized subscriptions and boosting customer loyalty.

Market Challenges

High Packaging & Transport Costs: Bottled water prices remain significantly higher than tap water, influenced by PET costs and logistical expenses.

Environmental and Regulatory Pressure: Elevated plastic waste generated from single-use PET bottles is prompting regional regulatory action and consumer backlash.

Intensifying Brand Competition: The market is fragmented, with global giants like Coca‑Cola (Arwa) and Nestlé (Sohat) competing against agile regional brands.

Infrastructure Constraints: In underdeveloped areas, limited bottling capacities, distribution challenges, and inconsistent quality controls can hinder market growth.

Competitive Landscape

Mai Dubai – Established by DEWA in 2012, the company leveraged its state backing and quality focus to capture market share in Gulf countries and tourism‑driven outlets.

Arwa – A Coca‑Cola-licensed brand since 1990, Arwa’s wide distribution in the UAE and Middle East, along with flavored extensions, positions it strongly.

Ambo – Ethiopia’s landmark mineral water brand, in partnership with Coca‑Cola Beverages Africa, exports to multiple MEA countries, enjoying historic brand equity.

Sohat – Lebanon’s leading mineral water (with 35% market share) is recognized for its pristine spring source and Nestlé-backed modernization.

Future Outlook & Growth Opportunities

Although precise CAGR figures were not disclosed, the MEA bottled water sector is expected to expand significantly through 2028. Key growth avenues include:

Desalination-backed bottling in Gulf countries to combat freshwater scarcity.

Scaling PET recycling infrastructure to support eco-friendly packaging initiatives.

Expanding premium segments by leveraging natural spring sources and export potential.

Deepening rural reach via sachet water solutions in Sub-Saharan Africa, where formal bottling infrastructure is limited.

Enhancing D2C subscriptions and digital retail, especially in urban and expatriate communities.

Conclusion

The Middle East & Africa Bottled Water Market is at an inflection point, fueled by environmental constraints, health-driven consumption, and premiumization trends. Key brands like Mai Dubai, Arwa, Ambo, and Sohat are strategically positioned to lead this transformation. Sustained growth, however, hinges on balancing market expansion with sustainability initiatives and infrastructural investments. For decision-makers and investors, this sector offers compelling opportunities underpinned by demographic growth and evolving consumer preferences.

Want detailed insights on this market? Download the Sample Report Now!